Corporate tax cuts have long been a contentious issue, particularly in the wake of the 2017 Tax Cuts and Jobs Act, which significantly altered the landscape of corporate tax policy in the United States. This legislation aimed to stimulate business investment by slashing the corporate tax rate from 35% to 21%. Supporters argued that these corporate tax cuts would unleash economic growth and lead to higher wages for employees. However, a recent analysis by Harvard economist Gabriel Chodorow-Reich highlights the complexities surrounding corporate tax cuts, suggesting that while there were some modest gains in investment, they were not enough to counter the substantial decline in tax revenue. As Congress prepares for another tax debate, understanding the ramifications of these tax cuts and their impact on the economy will remain critical for informing future policies.

The discussion surrounding reductions in taxation for corporations often extends beyond mere percentages, encompassing a broader conversation about economic policy and fiscal responsibility. Recent analyses of the 2017 tax reforms, often referred to as corporate tax relief measures, have sparked debates over their effectiveness and long-term sustainability. Some argue that these concessive fiscal policies encourage firms to invest more, potentially boosting the economy, while others point to the troubling decline in government tax revenue. The ongoing dialogue is further complicated by varying interpretations of data, such as those presented in the Chodorow-Reich analysis, underscoring the necessity of a robust examination of how corporate taxation shapes the investment landscape and public services. As lawmakers grapple with the expiration of key provisions, the choices they make will have lasting implications for both businesses and taxpayers.

Understanding the Impact of the 2017 Tax Cuts and Jobs Act

The 2017 Tax Cuts and Jobs Act (TCJA) implemented sweeping changes to the corporate tax policy in the United States, primarily aiming to stimulate economic growth through tax cuts. However, the reality of its impact on business investments and overall economic health has sparked extensive debate among economists and political figures alike. Evaluating the TCJA reveals mixed outcomes; while it sought to encourage business investment by lowering corporate tax rates from 35% to 21%, analyses show that the resultant increase in investment was modest at about 11%—far less than proponents had anticipated.

Critics often argue that the TCJA’s provisions disproportionately favored large corporations at the expense of increased tax revenue necessary for funding public programs. Gabriel Chodorow-Reich’s analysis demonstrates that while the law improved capital investments to some extent, this was overshadowed by a significant decline in tax revenue. As economists scrutinize the data, it becomes apparent that the narrative surrounding tax cuts is more complex than the traditional belief that they universally benefit the economy.

The Debate Over Future Corporate Tax Cuts

As Congress approaches a crucial tax debate scheduled for 2025, the efficacy of the TCJA remains under the microscope. With certain key provisions of the TCJA poised to expire, including those affecting corporate tax rates, both Republicans and Democrats are advocating for diverse solutions. Vice President Kamala Harris’s push for raising corporate tax rates aims to finance other social initiatives, while former President Donald Trump’s stance on maintaining and possibly lowering tax rates focuses on further stimulating business growth. This dichotomy in perspectives underscores the ongoing contention regarding corporate tax cuts.

Current economic conditions, especially following the COVID-19 pandemic, add a layer of complexity to the discussion. Chodorow-Reich’s findings highlight that, despite an initial drop in corporate tax revenue post-TCJA, there has been an unexpected recovery, with corporate profits exceeding forecasts. This resurgence raises questions about how corporations are responding to tax policies and whether future adjustments will effectively balance the needs of businesses with the government’s revenue requirements.

The Need for Intelligent Solutions in Corporate Tax Policy

The analysis conducted by Chodorow-Reich and his colleagues yields valuable insights into how corporate tax policy can be refined to serve the greater good. The economists emphasize that while lower statutory rates were intended to foster growth, targeted expensing provisions have proven more effective in driving significant investments. This acknowledgment calls for policymakers to re-evaluate the parameters of corporate taxation to embrace a more nuanced approach, one that prioritizes meaningful growth while also addressing the pressing need for government revenue.

The complexity surrounding corporate taxation prompts skepticism over simplistic narratives linking tax cuts directly to economic prosperity. By promoting a deeper understanding of the relationship between tax policy and business behavior, the aim should center on creating frameworks that encourage innovation and investment, ultimately benefiting the workforce. Such intelligent solutions could pave the way for legislation that not only champions corporate interests but also secures necessary tax revenue to enhance public programs.

Analyzing Wage Growth Amid Corporate Tax Changes

Amid the discussions of corporate tax cuts, wage growth presents another critical area of inquiry. Previous predictions suggested that the TCJA would significantly increase wages, estimating gains ranging from $4,000 to $9,000 per full-time employee. However, Chodorow-Reich’s findings reveal that the actual increase was substantially lower, closer to $750 annually. This discrepancy raises essential questions about the real beneficiaries of corporate tax reforms and whether the anticipated advantages have been realized in wage growth for the average worker.

With corporate profits rising following the TCJA, many anticipated that employees would share in that success through higher wages. The data indicates a less optimistic reality, suggesting that while tax policies may enhance corporate profits, the transfer of those benefits to workers is not guaranteed. Policymakers need to consider how tax reforms can be strategically employed to ensure that wage growth keeps pace with corporate earnings, fostering a more equitable economic landscape.

Corporate Tax Strategies and Business Innovation

One of the intended effects of the TCJA was to encourage corporate investment in innovation, with provisions allowing companies to write off expenses related to new capital and research immediately. This strategy aimed at spurring firms to invest heavily in technology and improvements that would ultimately benefit the economy. However, the mixed results documented in Chodorow-Reich’s analysis indicate that while investment did rise, the overall impact on long-term innovation capabilities is still questionable.

This situation poses a critical challenge for legislatures aiming to foster a robust business environment. As businesses recover and adapt to new economic realities, tax policies should not only incentivize immediate returns but also nurture sustained innovation that demands both patience and investment in human capital. Crafting a corporate tax framework that aligns immediate tax breaks with long-term growth strategies is essential for ensuring that businesses invest not just in profits, but in the future of their labor force and the economy as a whole.

Exploring the Global Competitiveness of U.S. Corporations

The competitive landscape of corporate taxation on a global scale has evolved dramatically since the TCJA was enacted. In the analyzed period, the U.S.’s corporate tax rate was among the highest in the industrialized world. However, international pressure has prompted a wave of tax reforms from various nations, markedly affecting U.S. corporations that operate globally. Chodorow-Reich notes that the changes aimed to align U.S. tax rates more competitively with those of other countries, yet questions remain regarding their efficacy in maintaining America’s economic supremacy.

The removal of ultra-low corporate tax rates in countries like Ireland has also influenced U.S. corporations to re-evaluate their profit reporting strategies. Multinationals may now channel profits back into the U.S., which reflects a shift in corporate tax behavior prompted by legislative changes domestically and abroad. Understanding these dynamics is crucial for developing tax policies that not only prioritize competitiveness but also ensure corporations contribute fairly to national tax revenues.

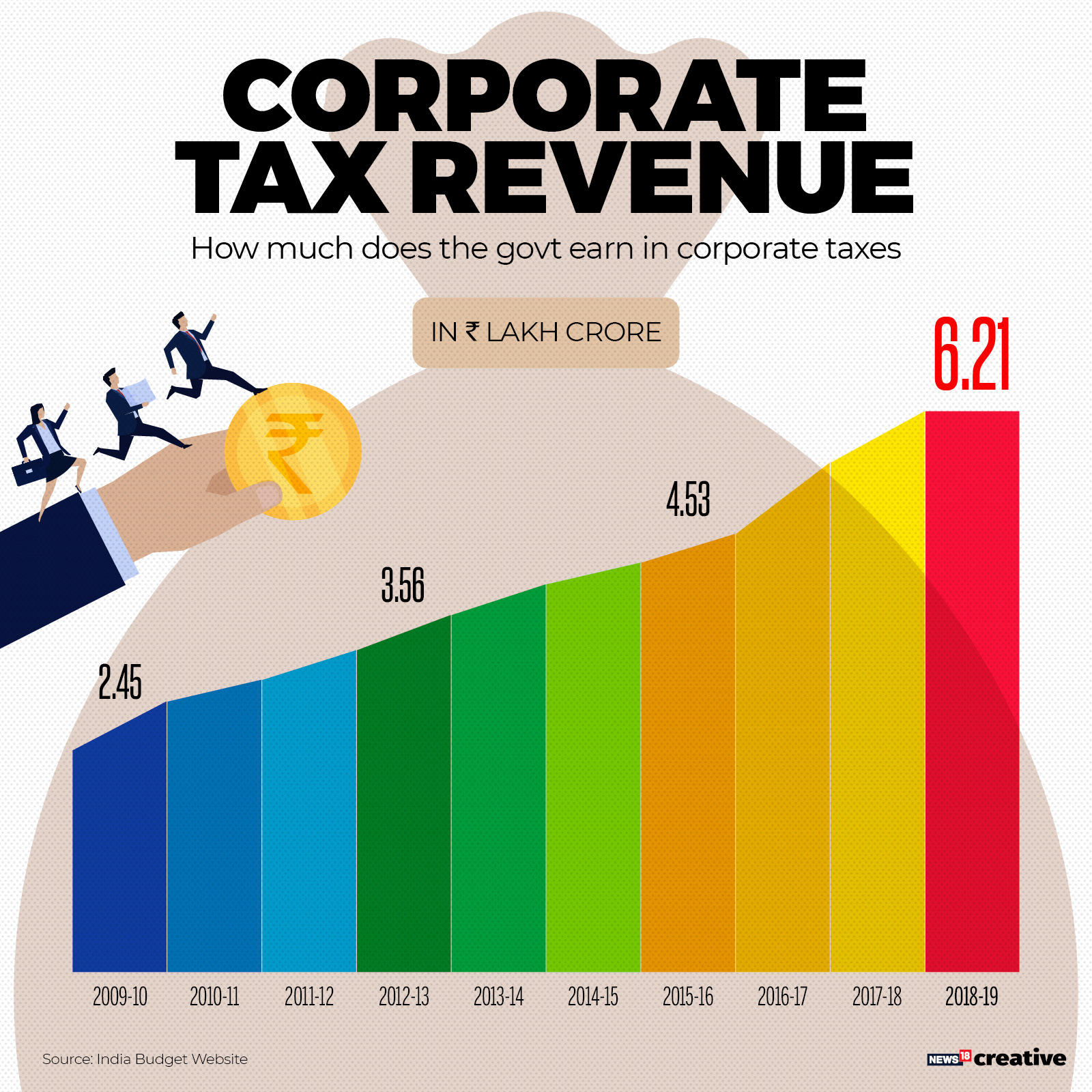

Examining Corporate Tax Revenue Decline

One of the most significant impacts of the TCJA has been the pronounced decline in corporate tax revenue, which saw an initial drop of 40% following the implementation of the law. This dramatic decrease necessitated a reevaluation of federal budget strategies and led to a potential crisis in funding for essential government services. As economists analyze the short-term and long-term implications of this decline, it raises pressing questions about fiscal responsibility and the sustainability of current tax policies.

The recent recovery in corporate tax revenue since 2020 highlights the complexity of these dynamics. With surpassing business profits post-pandemic, some narratives lean towards corporations thriving under the new tax structure, yet deeper analysis is vital to gauge the overall impact on government funding. Future tax initiatives must factor in the learnings from the TCJA’s trajectory to create a sustainable revenue model that serves both corporate interests and public needs.

The Role of Public Opinion in Tax Policy Changes

Public opinion plays a crucial role in shaping tax policies, particularly as impending elections heighten discussions around corporate tax rates. As seen with the TCJA, the polarization around tax cuts—where one side argues for lower rates to stimulate growth, while the other advocates for higher rates to ensure equity—reflects varying public sentiments and priorities. Understanding the nuances behind these opinions can empower lawmakers to draft more effective policies that align with the electorate’s needs.

Amid the contentious atmosphere surrounding tax reforms, engaging with constituents regarding their views on corporate taxation becomes critical. By fostering a dialogue focused on transparent data, such as those from Chodorow-Reich’s study, policymakers can bridge the gap between theoretical projections and public expectations, resulting in more informed legislative outcomes. Ultimately, a participatory approach to tax policy can guide reform efforts to encourage broader economic growth while ensuring fairness in tax contributions.

Future Directions in Corporate Tax Legislation

As corporate tax discussions take precedence in the lead-up to Congress’s tax debate in 2025, a pivotal question arises: what should the future of corporate taxation look like? Chodorow-Reich’s insights suggest a balanced approach where statutory rates may be raised while reinstating effective expensing provisions—striking a balance between revenue generation and encouraging business investments. This dual strategy could enhance the government’s fiscal health without stalling economic growth.

Moving forward, policymakers need to leverage empirical evidence to guide their decision-making processes. The TCJA’s legacy provides a rich data set to understand the consequences of tax policy changes, thus empowering lawmakers to craft future legislation that maximizes economic benefits while maintaining necessary public financing. By learning from past reforms, new tax initiatives can aim for an equitable landscape where corporate success complements the social fabric of the nation.

Frequently Asked Questions

What are the key effects of corporate tax cuts as per the Tax Cuts and Jobs Act?

The Tax Cuts and Jobs Act (TCJA) implemented significant corporate tax cuts by reducing the federal corporate tax rate from 35% to 21%. This change was intended to stimulate business investment and drive economic growth. According to research by Gabriel Chodorow-Reich and others, while there was a modest increase in capital investments by about 11%, the increase in wages was considerably lower than expected, estimated at approximately $750 per year for full-time employees.

How did corporate tax cuts impact tax revenue according to Chodorow-Reich’s analysis?

Chodorow-Reich’s analysis indicates that corporate tax revenue initially dropped by 40% after the implementation of the TCJA. Although revenue began to recover starting in 2020, it still showed a significant decline overall due to the drastic cuts introduced by the tax policy, which was projected to reduce federal corporate tax revenue by $100 to $150 billion annually over the next decade.

What was the rationale behind the corporate tax cuts under the TCJA?

Proponents of the corporate tax cuts under the TCJA believed that lowering the statutory rates would incentivize businesses to invest more in capital, thereby stimulating growth and creating jobs. The expectation was that increased business investment would lead to higher corporate profits, which could ultimately benefit taxpayers through elevated wages and economic expansion.

What did the Chodorow-Reich analysis say about the relationship between corporate tax policy and business investment?

The Chodorow-Reich analysis concluded that firms do respond to corporate tax policy, notably highlighting that expiring provisions for expensing new investments were more effective in driving investments compared to traditional rate cuts. This suggests that targeted tax incentives, such as immediate write-offs for capital expenses, might be more beneficial for encouraging business development.

What should lawmakers consider regarding corporate tax policy reforms in the future?

As noted by Chodorow-Reich, lawmakers could consider raising statutory rates while reinstating expensing provisions to balance the need for increased tax revenue with incentives for business investment. This approach may facilitate a beneficial cycle where increased investments drive up demand for labor, leading to higher wages for employees.

How did corporate profits respond in the aftermath of the TCJA, post-pandemic?

Following the implementation of the TCJA, corporate profits surged unexpectedly during the pandemic, outpacing forecasts. Chodorow-Reich suggested that factors such as supply chain adjustments and shifts in corporate profit reporting might have contributed to this trend, as many companies began registering higher profits in the U.S. due to the lower tax rate.

What are the main criticisms surrounding the corporate tax cuts enacted by the TCJA?

Critics argue that the corporate tax cuts led to a significant decline in government revenue without delivering the promised substantial wage increases for workers. The analysis by Chodorow-Reich indicated that the wage growth resulting from these tax cuts was much less than predicted, pointing to a need for more thorough assessment of the impacts of corporate tax policy.

| Key Point | Details |

|---|---|

| Corporate Tax Cuts | The 2017 Tax Cuts and Jobs Act (TCJA) reduced the corporate tax rate from 35% to 21%, designed to stimulate business investment. |

| Economic Impact | Analysis shows that while there was an increase in corporate investments by about 11%, the wage growth was significantly lower than expected. |

| Partisan Debate | The upcoming 2025 tax battles are marked by differing perspectives from Republicans and Democrats, with arguments for both increasing and cutting corporate tax rates. |

| Revenue Effects | Post-TCJA, corporate tax revenue initially dropped by 40% but began to recover significantly as business profits climbed unpredictably. |

| Future Proposals | Chodorow-Reich suggests reinstating expensing provisions, which shows better investments, while potentially raising statutory rates for balanced revenue. |

Summary

Corporate tax cuts have become a central topic of debate as lawmakers prepare for a tax battle in 2025. The findings of recent studies question the effectiveness of the TCJA’s reductions in stimulating significant wage growth despite modest gains in business investment. With a divided view on corporate tax policies among lawmakers, the ongoing discourse will likely define future economic policies and their implications for fiscal responsibility.